I am not proud of this, but I have mostly been ignoring the advice to “look before you leap” when it comes to investing. My typical investment journey goes like this: I see some arguments for investing in some asset; I jump right into investing in it; a few months later I decide I don’t want that asset; then I figure out how to course correct. It happened with gold. It happened with Nifty 50. It may probably happen with active equity funds in the near future.

This blog post is about another such story.

Accumulating gold

When I decided to remove gold from my investment portfolio, I thought that investing in equity+debt was a good way to accumulate purchasing power to buy gold in future. If equity appreciates more rapidly than gold does, I thought, investing in equity was better than investing in gold.

But now I have a different point of view. If the end goal is to buy gold, accumulating gold slowly over time is likely a better approach than investing in equity.

The goal based investing framework recommends taking just enough risk to meet our financial goals. You don’t put all your money in fixed income because it’s going to be very difficult to retain your money’s purchasing power that way. You need to take more risk. So you add equity to your portfolio. But you don’t hold 100% or 80% equity for long since the added volatility can make it difficult to meet your financial goals. An investor following the goal based investing framework would start with relatively high equity exposure, but regularly keep reducing equity exposure to progressively reduce risk.

Investing to buy gold is tricky. Gold is just as volatile as equity is. But if equity prices fall, gold price may rise and vice versa. Gold’s price appreciation is also usually faster than fixed income’s growth. Given these, holding equity and/or fixed income assets to eventually buy gold sounds risky. it’s arguably less risky to just buy [investment] gold and hold it until we need to buy [consumption] gold. At the time of buying gold for consumption, we can sell the investment gold, and we’ll have just enough money. By holding gold as investment, we nullify the impact of gold’s price volatility.

Using sovereign gold bonds to accumulate gold

Sovereign gold bonds (SGBs) are issued by the Reserve Bank of India (RBI). These bonds have a fixed tenure of 8 years. A bond that was issued on 1-May-2021, for example, will mature on 30-April-2029. Each bond represents 1 gram of gold. On maturity, the current price of gold will be paid to the bondholder. If gold price had appreciated in these 8 years, the bondholder need not pay any tax on the capital gain, which is a good incentive for most people.

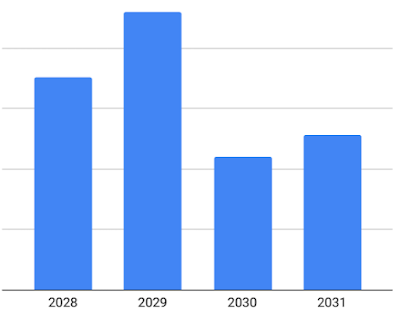

Indian weddings make use of gold. A nontrivial amount of gold is needed if you are the bride’s side. (The groom’s side usually doesn’t need as much gold.) I roughly know when our girl children will get married, so it’s easy to tell how much gold we’ll need when. In my investment tracker spreadsheet, I plot the maturity of our SGBs as a graph like this:

This graph tells me how many of our SGBs mature in a given year. This gives me clarity on exactly how much gold we can buy in that year. Accumulating SGBs is a convenient and less risky way to accumulate gold if the end goal is to buy consumption gold.

No comments:

Post a Comment