We bought a house in February 2023. My original plan was to sell my Google shares to fund the house purchase. I have always had “too much” exposure to Google shares. Selling Google shares to buy the house was a way to reduce the concentration risk. But by the time we finalised a house, the price of Google shares had fallen pretty badly.

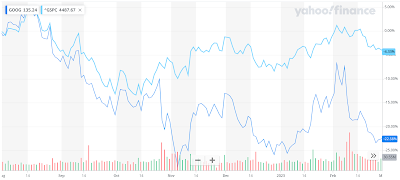

You can see the stark difference between the left half of the following price graph and the right half.

|

| Google share price has appreciated by 21.42% in the last 12 months. But it was in the negative territory for the first 9 months. |

|

| Between August 2022 and February 2023, Google share price fell by 22.58%! |

When we knew which house we were buying and how much money we needed, Google shares were trading for around $90. I felt it was too low a price to be selling at. I changed the plan and found a different way to raise funds. It felt unnerving when I did that because selling Google shares had always been the plan. Changing the plan in the final weeks is essentially dancing to the tune of the market — something I want to avoid.

$GOOG’s performance since then is nothing short of amazing: almost 50% growth in the last 6 months! It made up for the previous ~20% loss and appreciated further to post a +20% increase year-over-year!

|

| Between March 2023 and September 2023, Google share price grew by 49.47% |

Lessons learnt

- Price swings of 2% or 3% in a day is a regular event. 20% or 50% up/down in a year is also fairly common. Direct equity investors should accept this bumpy ride.

- What does that mean in practice? You may have heard people advising to not lose hope when the price falls. But the reverse is also true: we should not celebrate if there is a rally and the price is going up. The price can fall any day.

- Well-diversified mutual funds are a much better alternative for those who don’t like so much volatility. For example when investing towards a financial goal. Directly holding 20+ diversified stocks is not a comparable alternative because deciding how much of what to sell may not be straightforward.

- Direct equity investors need to be nimble-footed. They should be willing to change plans when needed. It would have been a bummer if I had sold off my Google shares for $90.

- In addition to having the willingness to alter the plan, a direct equity investor should also have the ability to alter the plan. My situation would have been rough if selling Google shares was the only option.

- This one I am not so sure about, but… maybe I am better at making investment decisions than I give myself credit for. (Or maybe I just got lucky. What if $GOOG had never recovered? What if $GOOG kept falling?)