You want to invest in mutual funds, but you don’t know which of the thousands of available funds is right for you. The easiest thing to do is just look at historical returns and pick one that has performed well in the past. That’s pretty much what I did when I started investing in mutual funds a few years ago. Unsurprisingly, the returns weren’t as mind-blowing as I had expected.

Fast forward to 2020, I am now a Kuvera customer. (Plug: join using my referral code

■

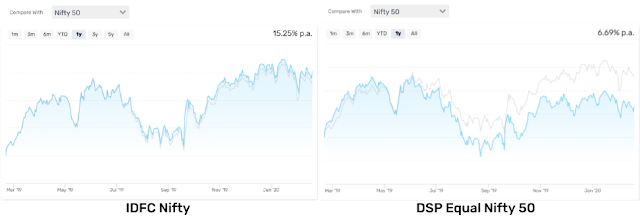

In October 2018, Kuvera changed their recommended funds. In October 2018, they started recommending DSP Equal Nifty 50 instead of IDFC Nifty. I compared the facts and performance of these 2 funds, and it was surprising how unattractive the DSP fund looked to a novice investor like me.

In the past year, the IDFC fund has given an impressive 15.25% return while the DSP fund has given a mere 6.69%. The DSP fund’s return is below the benchmark return, actually!

The fact that the DSP fund is underperforming the benchmark is reflected in its “info” statistic. The IDFC fund has 0.8 for “info” while the DSP fund has -0.04! The IDFC fund wins in other attributes too: it has a cheaper expense ratio (0.24% vs 0.38%) as well as barely less volatility (14.14% vs 14.25%).

How then is the DSP fund better than the IDFC fund? They mention 3 reasons:

Lower concentration of financials

This becomes obvious if you look at the stocks held by these funds. The IDFC fund holds HDFC Bank shares for 10.6% of its value. In other words, you would be buying HDFC Bank shares roughly worth ₹10.60 if you were to buy the IDFC fund for ₹100. Intuitively, that is not something you’d want to do if you want to diversify your investments. But there’s more than just intuition.

Historic EW premium

I think the “EW” refers to “equal weight” here. The DSP fund distributes the money roughly equally between every share in the Nifty 50 basket. While intuitively this is a good diversification strategy, apparently this has yielded better returns historically. Gaurav Rastogi, CEO of Kuvera, states in a comment:

What are my takeaways from this?

Fast forward to 2020, I am now a Kuvera customer. (Plug: join using my referral code

JK1P3 and get 100 Kuvera coins for free.) In addition to providing a well thought-out investment platform for free, Kuvera has written quite a bit about how to think about investing and wealth management. From the experience using Kuvera and reading about the thinking behind their decisions, I think I am starting to see some of the intricacies in choosing a good fund.■

In October 2018, Kuvera changed their recommended funds. In October 2018, they started recommending DSP Equal Nifty 50 instead of IDFC Nifty. I compared the facts and performance of these 2 funds, and it was surprising how unattractive the DSP fund looked to a novice investor like me.

In the past year, the IDFC fund has given an impressive 15.25% return while the DSP fund has given a mere 6.69%. The DSP fund’s return is below the benchmark return, actually!

The fact that the DSP fund is underperforming the benchmark is reflected in its “info” statistic. The IDFC fund has 0.8 for “info” while the DSP fund has -0.04! The IDFC fund wins in other attributes too: it has a cheaper expense ratio (0.24% vs 0.38%) as well as barely less volatility (14.14% vs 14.25%).

How then is the DSP fund better than the IDFC fund? They mention 3 reasons:

- Lower concentration of financials

- Historic EW premium

- Buy low–sell high in a systematic way

Lower concentration of financials

This becomes obvious if you look at the stocks held by these funds. The IDFC fund holds HDFC Bank shares for 10.6% of its value. In other words, you would be buying HDFC Bank shares roughly worth ₹10.60 if you were to buy the IDFC fund for ₹100. Intuitively, that is not something you’d want to do if you want to diversify your investments. But there’s more than just intuition.

Historic EW premium

I think the “EW” refers to “equal weight” here. The DSP fund distributes the money roughly equally between every share in the Nifty 50 basket. While intuitively this is a good diversification strategy, apparently this has yielded better returns historically. Gaurav Rastogi, CEO of Kuvera, states in a comment:

The reason we choose DSP Equal Weight Nifty fund instead of a plain vanilla Nifty index (IDFC) fund is because Equal Weight indices have outperformed their plain vanilla indices globally and in our back test in India as well on a risk adjusted basis.■

What are my takeaways from this?

- Past returns are useful data, but comparing the returns of 2 funds may not give us the full picture.

- Understanding how a fund is managed such as how they choose shares, the objective of the fund, etc are important. Investors should understand what the fund manager does with our money.

- Because most of us don't have the time or skill needed to study the mutual fund options, following the recommendations of good financial advisors is an easy shortcut to picking good investments. (How you tell if an advisor is good, I have no idea!)